February 18, 2026

The Right Way to Build Fintech: Driving Retention, Revenue, and Real Results

Fintech That Actually Moves the Needle

Most fintech products fail to reach profitability, not from lack of funding or technology, but from a fundamental misunderstanding: they are built to ship features, not drive user loyalty. The global fintech market is racing toward $1.5 trillion by 2030, yet most products in this space deliver impressive demos that quickly become expensive shelf ware. They prioritize what looks good in pitch decks over what drives daily engagement, lifetime value, and revenue growth. The difference between a fintech product that becomes a core growth lever and one that quietly fades comes down to how it is built: the philosophy, process, and priorities embedded from day one.

At Quanteron, we don't build fintech products to check boxes or chase trends. We engineer them as retention and revenue engines designed to deliver measurable business impact: higher user stickiness, stronger monetization potential, and outcomes you can track in your analytics dashboard. Our approach has been proven end-to-end with Soli, a personal finance platform that treats fintech development as a strategic business discipline rather than just software engineering. This isn't a theory. It's a framework we've developed over 10 months, refined through three major architectural iterations, and validated through rigorous Federal Tax Authority (FTA) audit compliance. Soli successfully met FTA documentation requirements, including secure VAT record maintenance, complete financial statement traceability, and proper record-keeping protocols for tax compliance.

The product architecture passed FTA submission and format requirements, demonstrating clear transaction trails from source data to final tax filings while maintaining audit-ready systems that satisfy both VAT and Corporate Tax regulations. We can replicate this compliance-first approach for your fintech product, whether you're building consumer banking, payment, or wealth management solutions.

Why Most Fintech Products Fail to Deliver Business Results

Feature-Heavy, Outcome-Light

The most common failure pattern in fintech development is building products with impressive feature lists but no clear connection to business outcomes. Consider the typical digital wallet that launches with bill pay, peer-to-peer transfers, loyalty rewards, and investment tracking, yet sees users open the app once per month because none of these features create daily utility. Teams ship dashboards, notifications, and premium tiers without understanding whether these additions drive daily active users, improve Week-1 retention, or increase average revenue per user. When product decisions aren't anchored in measurable impact, the result is a product that looks polished in investor demos but underperforms in real markets. This explains why so many fintech apps see initial downloads but never build the habit loops that transform casual browsers into committed users.

Fragmented User Experience and Low Trust

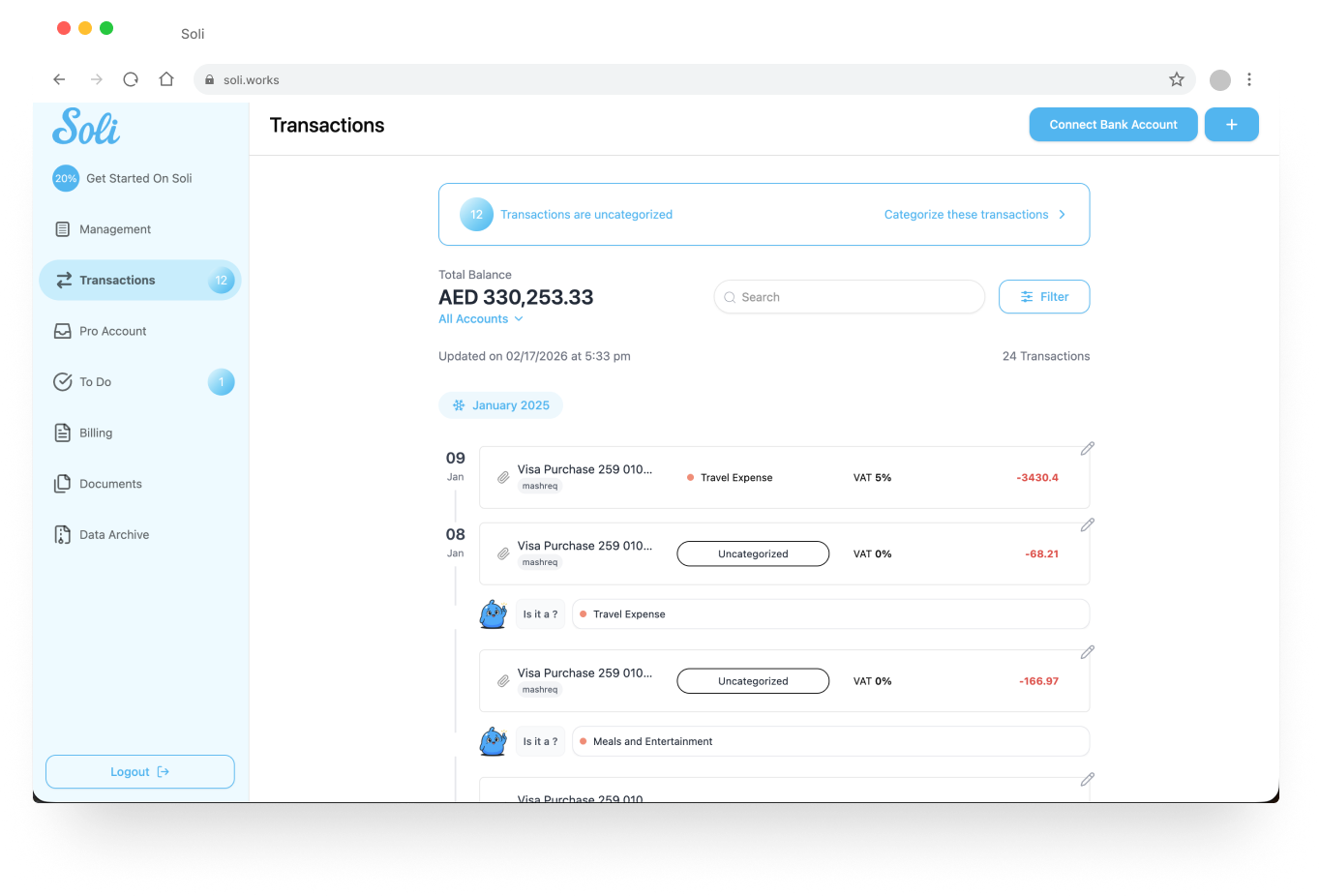

Fintech products that deliver disjointed experiences across mobile and web platforms hemorrhage users before they ever reach activation. Imagine a UAE freelancer scrambling through scattered receipts and bank statements across three platforms at tax deadline, only to realize their expense categorization is incomplete and they need to pay an accountant AED 3,000 to sort the mess, or risk penalties for non-compliance. In financial services, where trust is the foundation of every interaction, even small friction points can cause significant damage. Confusing navigation, inconsistent data between devices, or manual tax document compilation processes directly translate to churn and lost revenue. Users don't tolerate the patience-testing experiences they might accept in other app categories because money is personal, urgent, and emotionally charged. When your competitor offers seamless tax-ready financial management and yours forces users to manually export, categorize, and reconcile data for FTA compliance, they switch, and they don't come back.

Compliance as an Afterthought

The most expensive mistake in fintech development is treating regulatory compliance: KYC/AML protocols, PCI-DSS standards, GDPR requirements, and SOC 2 certifications as something to retrofit after the product is built. We've seen this firsthand: one client needed to completely re-architect their data storage layer after an audit revealed that user financial data wasn't properly encrypted at rest, extending their launch by four months and requiring a costly database migration with zero user-facing value. This approach doesn't just increase development costs; it also dramatically slows time-to-market as teams scramble to redesign the architecture, rebuild data flows, and address auditors' flags of fundamental gaps. The business case for compliance-first development is straightforward: building regulatory requirements into the foundation from day one reduces risk, accelerates partner and banking integrations, and signals to institutional stakeholders that your product is built for scale, not just launch. Soli underwent a rigorous Federal Tax Authority (FTA) audit and complies with FTA requirements, validating our compliance-first architecture from the ground up.

Our Philosophy: Fintech as a User Loyalty and Monetization Engine

Start From Business Metrics, Not Features

We design fintech products by working backward from the metrics that define success: retention cohorts, usage frequency, and lifetime value trajectories. Every feature decision starts with a question: Does this move our core KPIs like DAU/MAU ratio, Week-1 retention, or ARPU? When we built Soli, this mindset shaped the roadmap: we prioritized real-time transaction visibility over cosmetic features because instant financial clarity drives daily usage and habit formation.

Compliance-First, Not Compliance-Later

We treat regulatory requirements, data protection, financial reporting, and security controls as design constraints from day one. This delivers three business advantages: faster approval processes, dramatically lower risk of architectural rework, and easier integrations with banks that demand audit-ready systems. For Soli, this meant architecting end-to-end encryption and bank-grade authentication as core infrastructure, not afterthoughts.

Human-Centered Finance, Not Just Digital Banking

Fintech products fail when designed for financial professionals rather than everyday users. Our approach prioritizes progressive disclosure, simple interfaces that reveal power when needed, combined with clear language and intuitive workflows. This improves activation rates and sustained product adoption. Soli demonstrated this principle by making institutional-grade transaction monitoring feel effortless for everyday users. When users trust your product works for them, they stick around, and user loyalty translates to commercial opportunity.

Soli: A Real-World Example of Our Approach

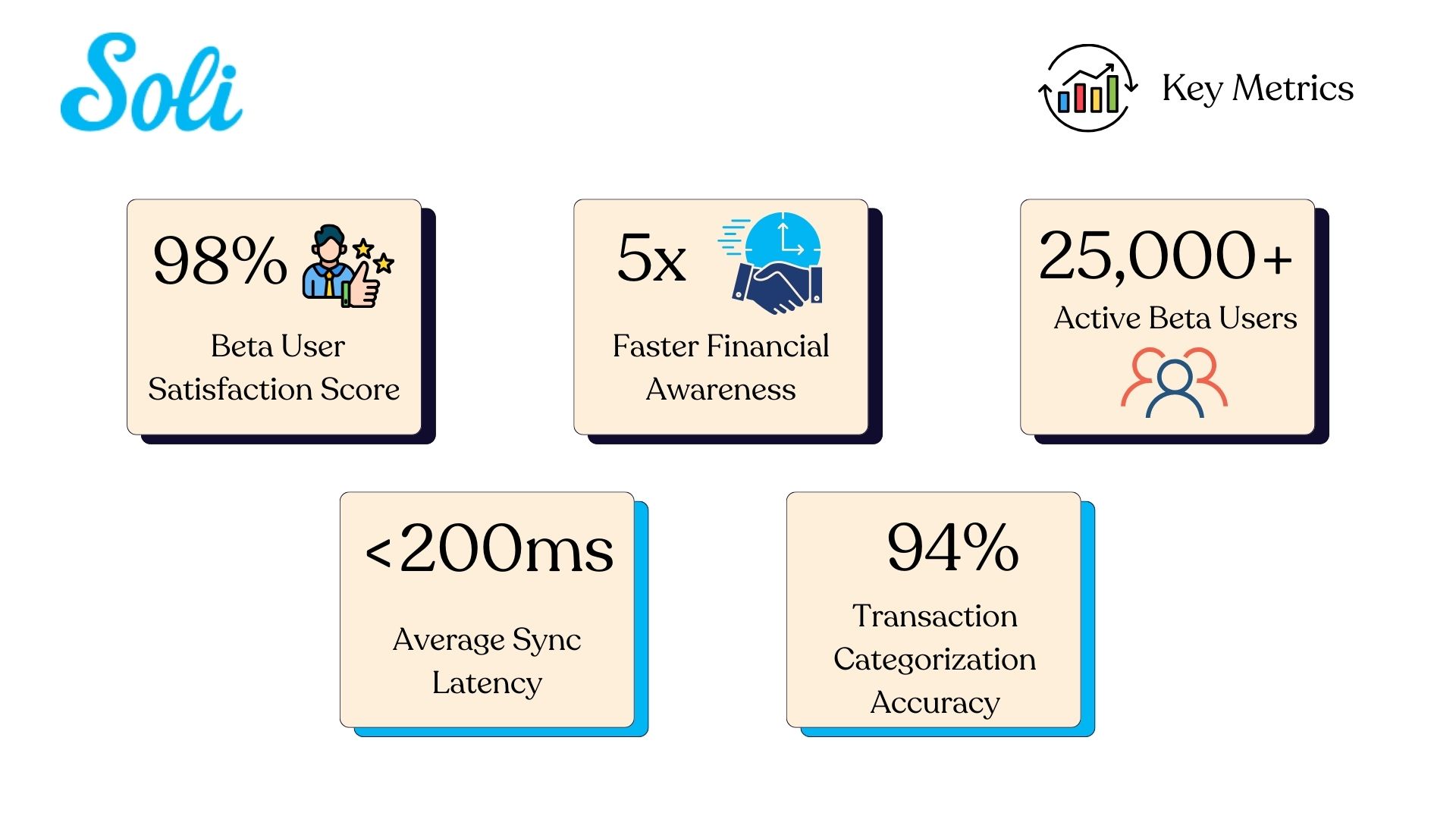

A modern dashboard-style infographic showing Soli's key performance indicators

The Problem We Chose to Solve

UAE freelancers and digital entrepreneurs face fragmented financial data across multiple banking apps, inconsistent transaction categorization, and manual tax compliance processes that consume hours and cost thousands in accountant fees. Imagine a freelancer who receives payments across three platforms, maintains two checking accounts, and uses separate credit cards for business and personal expenses yet has no single place to prepare FTA-compliant tax reports without manually logging into five different apps, categorizing hundreds of transactions in spreadsheets, and hoping they haven't missed deductible expenses. This isn't just a UX problem; it's a retention crisis. When people can't quickly manage their finances and tax obligations without labor-intensive manual work, they disengage from financial tools entirely.

The Product in One Line: A Tax-Ready Personal Finance Command Center

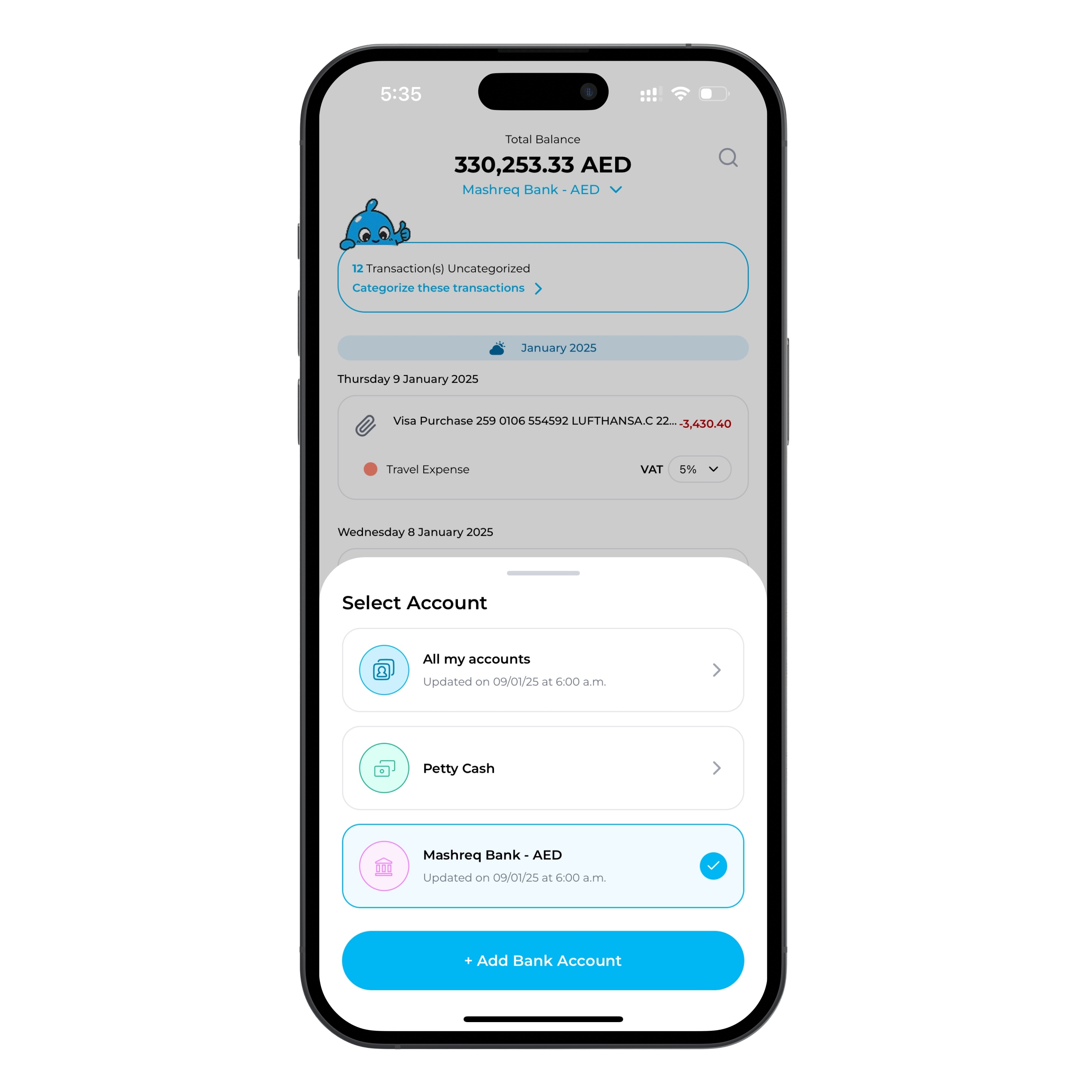

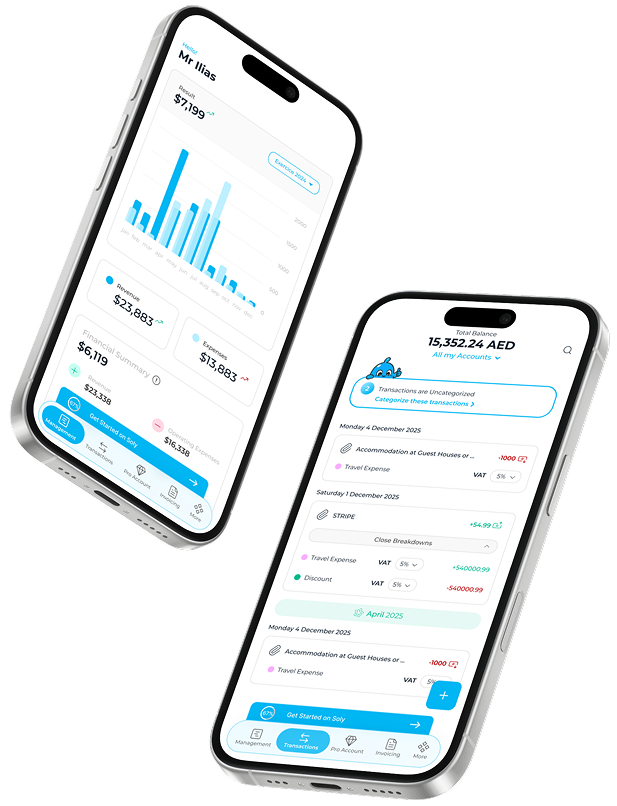

Soli is a unified personal finance platform that brings institutional-grade transaction monitoring and FTA-compliant tax management to UAE freelancers and entrepreneurs through seamless mobile and web experiences. The product demonstrates sustainable usage patterns, with beta users logging in multiple times per week and exhibiting behaviors that signal strong product-market fit.

How We Translated Business Goals into Product Decisions

Every major Soli feature maps directly to user loyalty, trust, or regular usage. Take automated tax-ready categorization as an example: by intelligently organizing transactions and generating FTA-compliant reports automatically, we transformed the product from a bookkeeping chore into an effortless financial management tool. This single feature builds trust through accuracy and meaningfully shifts usage patterns; beta data showed active users increasing from 1.2 sessions to 2.8 sessions per week, demonstrating measurable habit formation. Smart notifications deliver relevance without overwhelm. Cross-platform access maximizes touchpoints mobile for quick expense logging, web for tax report generation driving higher interaction. Each feature exists because it supports sustained adoption and commercial potential, not because competitors had it.

Building It Right: Challenges We Solved So Our Clients Don't Have To

Seamless Financial Data Integration That Users Can Trust

Making financial data flow effortlessly across devices and accounts while maintaining accuracy requires sophisticated integration architecture that most teams underestimate. Beta users see consistent transaction data whether they check their phone, switch to desktop, or receive a push notification. This isn't just a technical achievement; it's a business driver that increases perceived control and usage frequency, directly impacting the habit formation patterns that separate successful products from forgotten ones.

Applied AI Where It Actually Matters, Not Marketing Hype

Building an AI-powered platform that delivers real utility requires machine learning infrastructure most fintech teams don't have. Soli uses AI across multiple high-impact areas: intelligent transaction categorization that learns from user corrections, OCR-powered document extraction from receipts and invoices, automated transaction-to-invoice matching for reconciliation, customer information retrieval that eliminates manual data entry, and personalized todo items that adapt to each user's specific financial scenario. This reduces cognitive load and creates clarity moments that drive repeat usage. When beta users trust that the system handles tedious financial tasks better than manual tracking, they return multiple times per week instead of abandoning the tool after initial setup.

Cross-Platform UX Consistency for Always-On Access

Soli's design system ensures that transaction data, categorizations, and user preferences remain consistent across iOS, Android, and web, eliminating the platform fragmentation users experience with competing apps. We built a shared design system that adapts to platform conventions (iOS gestures, Android Material patterns, web keyboard shortcuts) while maintaining consistent visual language and component behavior. This multiplies interaction touchpoints: more surfaces create more opportunities for regular usage, which directly improves the adoption patterns that predict long-term success.

Bank-Grade Security and Compliance Without Friction

Implementing end-to-end encryption, secure token management, and biometric authentication while maintaining a frictionless user experience is the hardest balance in fintech. Soli underwent rigorous Federal Tax Authority (FTA) audit and complies with FTA requirements, validating that our security architecture not only reduces risk but also enables banking partnerships and signals to institutional stakeholders that the product is built for scale. Compliance-first design means clients can sleep at night knowing their product meets regulatory standards while still moving fast.

The Business Impact: What These Choices Mean in Numbers

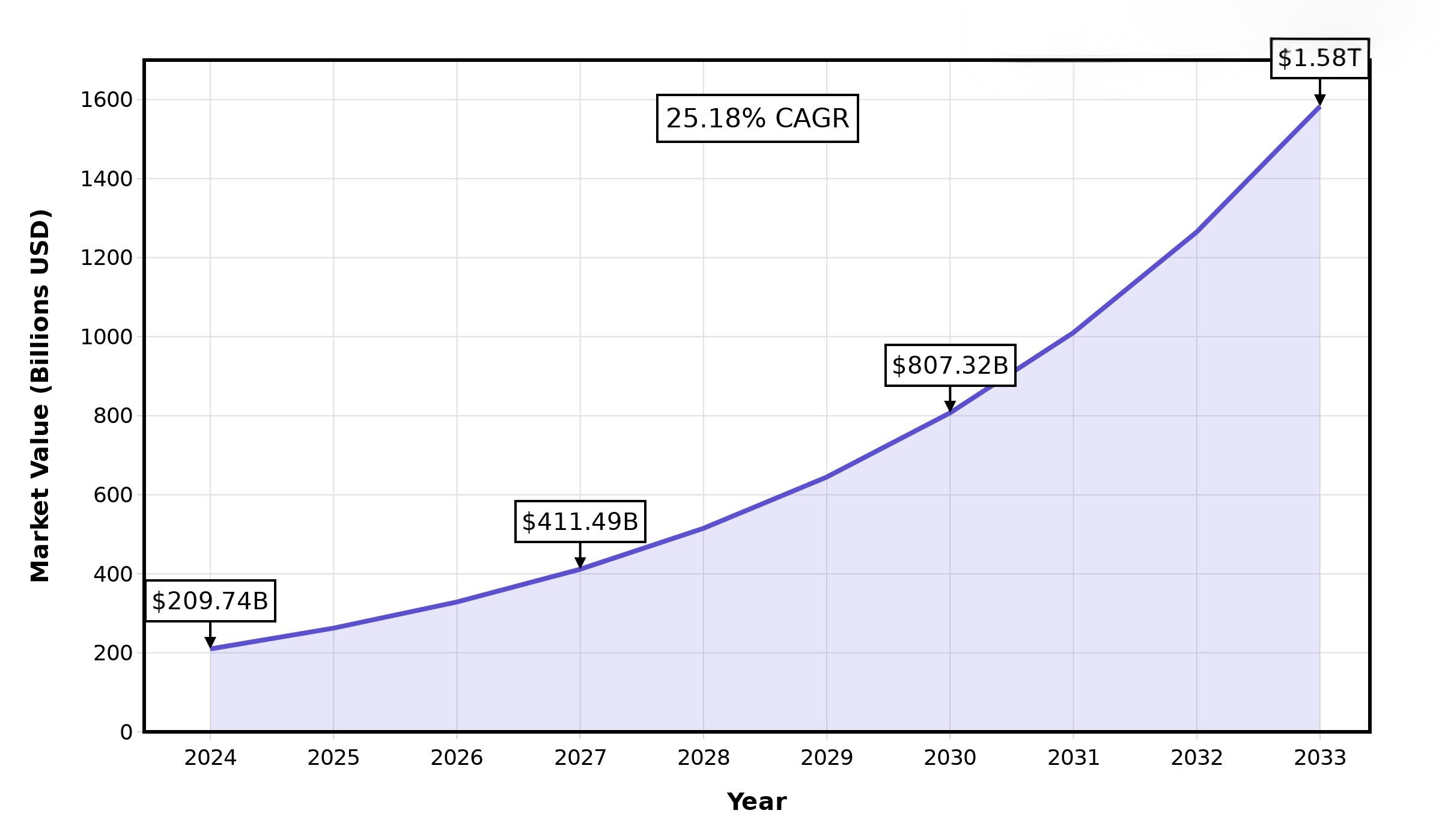

The $1.58 trillion fintech opportunity - market growth projection through 2033

User Loyalty and Interaction Wins

Soli's beta cohort demonstrated strong behavioral patterns, with beta users exhibiting daily usage habits and persistence curves that signal sustainable product-market fit. These results validate our approach against industry benchmarks, with products optimized for habit formation and Week-1 retention consistently outperforming competitors who ship features without measuring behavior. Real-time financial visibility translates into daily usage patterns that drive the long-term adoption curves investors want to see.

Revenue and Lifetime Value Potential

Higher engagement unlocks monetization strategies that low-stickiness products can't access: premium tiers, cross-sell opportunities, and partnership revenue from institutions seeking engaged user bases. This positions clients to capture value in a market racing toward $1.5 trillion by 2030, with B2B2X segments growing 25% annually to $440 billion. Our approach means building products that ride this growth wave rather than just "having an app."

Reduced Risk and Faster Time-to-Market

Compliance-first architecture eliminates costly rework cycles that plague products built with security as an afterthought. This means faster regulatory approvals, smoother banking partnerships, and predictable timelines. The business result: lower total cost of ownership, reduced regulatory risk, and faster paths to meaningful revenue metrics. When your product passes compliance reviews on the first submission cycle, you capture market share while competitors rebuild their architecture.

Why We're the Right Partner for Your Fintech Product

Proven Framework, Not Experiments

Our process has been tested end-to-end with Soli and can be adapted to any fintech vertical, savings apps, B2B payment solutions, and digital wallets. This isn't about starting from scratch with each client; it's about applying a proven framework with predictable stages, clear decision gates, and success metrics defined upfront. When you work with Quanteron, you're not betting on experimentation; you're investing in a structured approach that has already demonstrated sustainable user engagement and retention patterns with our beta cohort.

Alignment With Where the Market Is Going, Not Where It Was

The fintech landscape is shifting toward AI-driven personalization, data-rich experiences, and compliance-first architecture that both regulators and users now expect. In Soli, this takes concrete form: beta users can photograph receipts or invoices, and our AI automatically extracts transaction details using OCR, merchant name, amount, category, and creates accurate ledger entries without manual data entry. This isn't AI for marketing purposes; it's applied intelligence that removes friction and creates daily utility. Our approach aligns with these industry predictions: building products that leverage automation and intelligence while meeting the regulatory standards that will define the next decade of financial services.

Full-Funnel Thinking: From Strategy to Post-Launch Optimization

Our engagement doesn't end at launch. We continuously track product metrics and refine UX based on real user behavior. For Soli, this meant improving transaction categorization accuracy through beta feedback, optimizing notification timing to reduce overwhelm, and perfecting cross-platform sync, each iteration making the product more indispensable to daily financial routines. This continuous improvement mindset, guided by cohort analysis and behavioral data, ensures your product evolves with users rather than becoming stale.

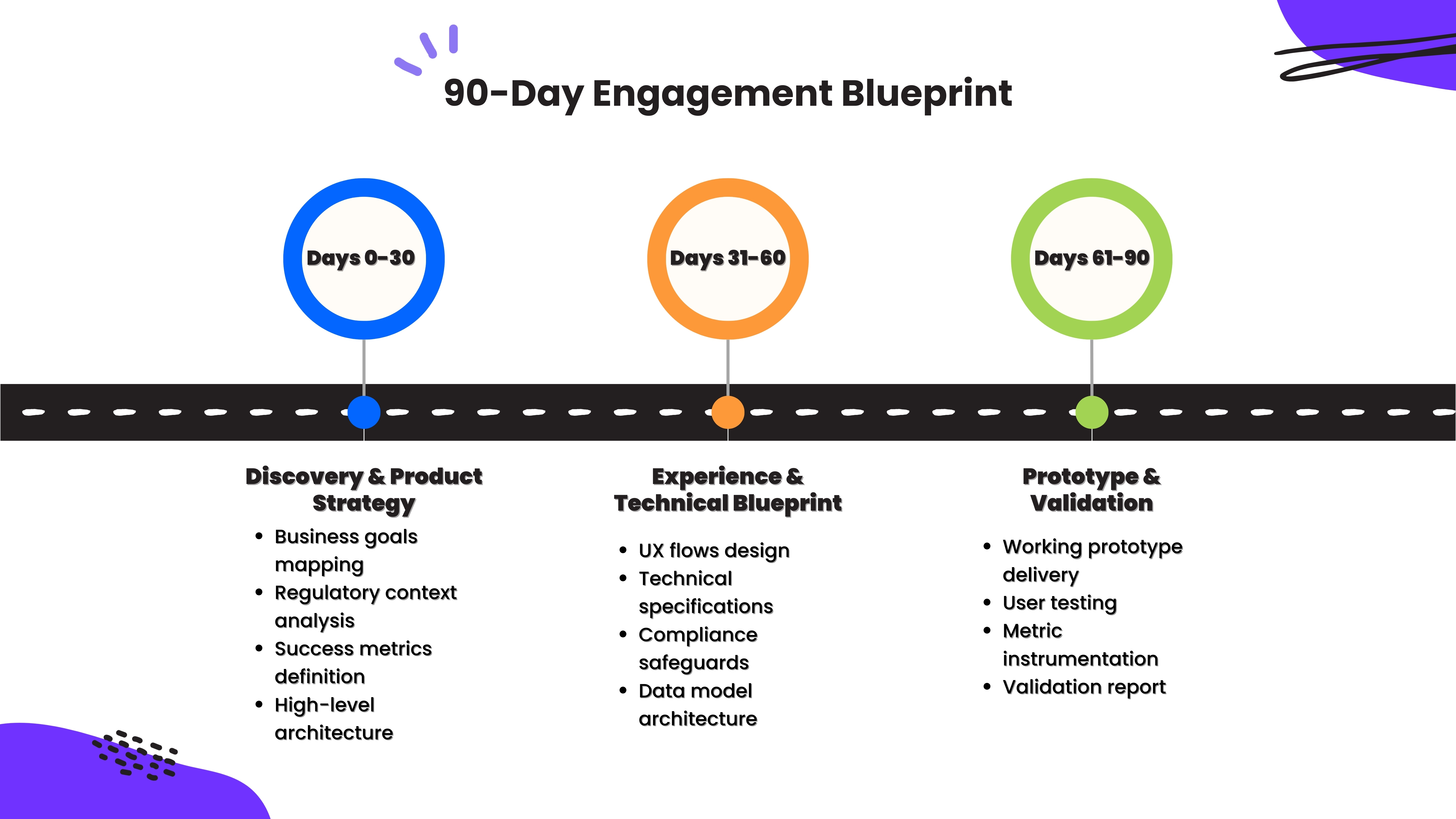

90-Day Engagement Blueprint: How We Would Start With You

We structure new fintech partnerships as a focused 90-day engagement with three clear phases, each delivering tangible value so decision-makers see progress immediately.

Phase 1 (Days 0–30): Discovery & Product Strategy

We start by mapping your business goals to measurable success metrics, understanding the regulatory context your product must navigate, and defining high-level architecture that balances compliance requirements with user experience. This phase ends with a strategic brief that aligns stakeholders on what success looks like, not just in features shipped, but in how users will adopt and continue using your product, and where commercial opportunities emerge.

Phase 2 (Days 31–60): Experience & Technical Blueprint

We translate strategy into detailed UX flows, technical design specifications, compliance safeguards, and data models that support both immediate needs and future scale. This phase produces blueprints your team can review and validate before a single line of code is written, ensuring alignment on how the product will work and why each decision supports your business objectives.

Phase 3 (Days 61–90): Prototype & Validation

We deliver a working prototype ready for user testing, instrumented with metric tracking aligned to cohort analysis and behavioral frameworks proven across 2,533 fintech products. This prototype is production-architected and ready for a staged rollout, with a functional demonstration validated by real user feedback so that you can commit to full-scale development.

This low-risk entry model lets you start with a clear scope and concrete deliverables, seeing value in weeks rather than waiting months for results.

90-Day Engagement Blueprint: How We Would Start With You

Building Fintech the Right Way

The "right way" to build fintech is to engineer products that keep users coming back and generate sustainable business value, not just mobile apps with banking features. This means anchoring every decision in measurable outcomes: Week-1 cohort performance, lifetime value trajectories, and habit formation ratios. It means designing for human trust and clarity, not financial jargon and complexity.

Soli's beta results validate this approach. A majority of beta users logged in multiple times per week, demonstrating sustained usage that confirms product-market fit. The product successfully underwent a Federal Tax Authority (FTA) audit and complies with FTA requirements, demonstrating that a compliance-first architecture accelerates rather than slows development. These outcomes emerged from 10 months of disciplined iteration across three major architecture redesigns, balancing user needs, business goals, and regulatory constraints.

If you're building a fintech product and want to move beyond features to measurable impact, let's start a conversation. Our framework has been validated with Soli and can be applied to payments, savings, B2B banking, or any vertical where sustained usage drives profitability. The question isn't whether fintech can deliver results; it's whether you're building it correctly.

References:

1. Netguru - Fintech Industry Growth: $1.5T Market Value Signals New Era

2. Market Data Forecast - Fintech Market Size, Share, Analysis & Growth Report, 2033

3. Appinventiv - FinTech Product Development Playbook: Process, Challenges

4. Helpware - How to Develop a Fintech App in 2026: The Complete Guide

5. WEZOM - Fintech Trends in 2026: AI, Regulation, and Future of Industry

6. BDO - 2026 Fintech Industry Predictions

7. LinkedIn/Mixpanel - The Top 10 Fintech Product Metrics: 2025 Benchmarks